Fear. Fear of the unknown. Fear of public speaking. Fear of death. Fear drives all of us in our decision-making process because it is encoded in our DNA. Every living, breathing thing instinctively evaluates threats to self-preservation first before any aspirational desires can be pursued.

In a reference to a recent study published by The Transamerica Center for Retirement Studies, several data points from the survey stand out relating to retiree sentiment concerning their greatest fears.

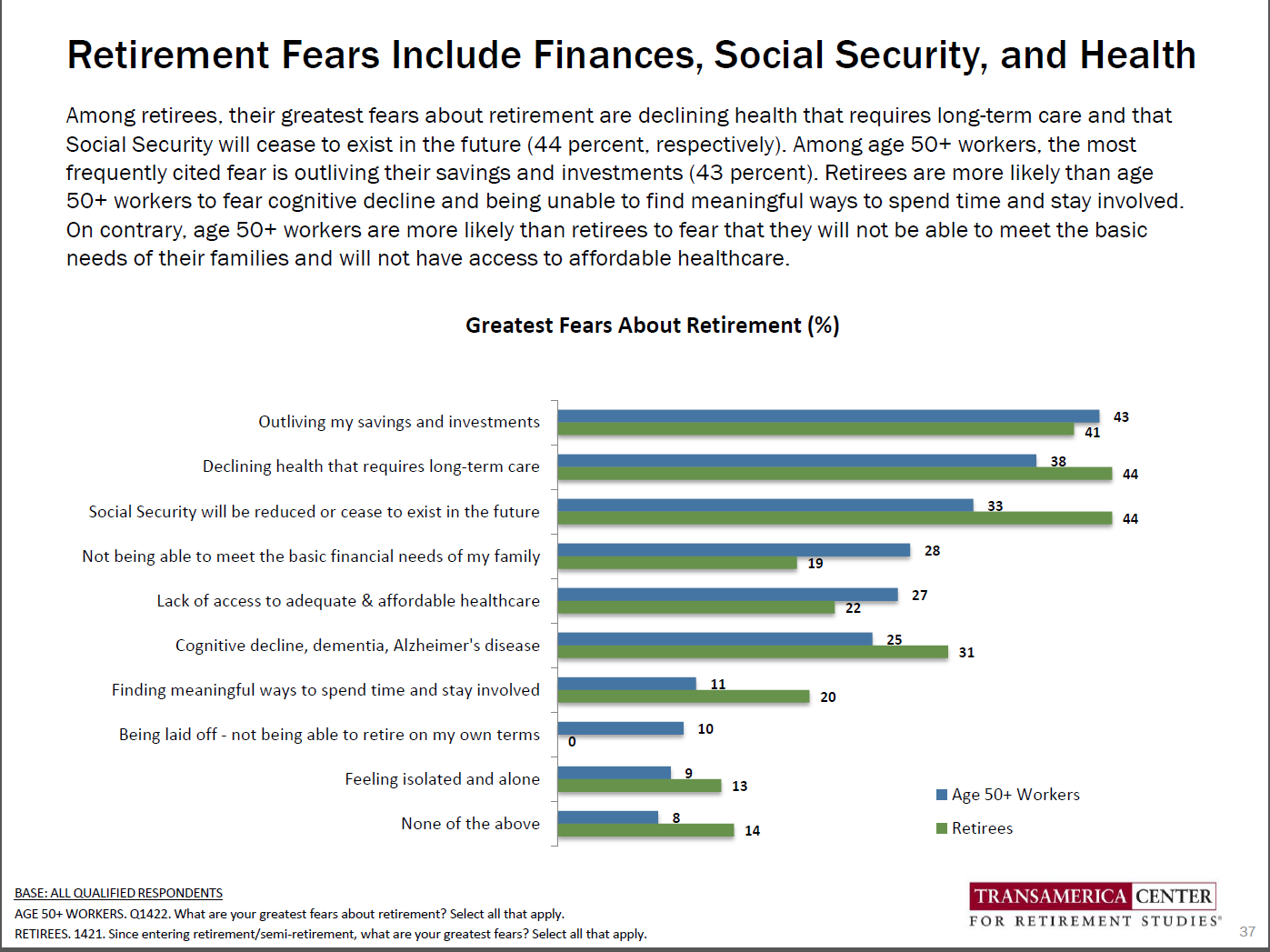

Source: Transamerica Center for Retirement Studies

Source: Transamerica Center for Retirement Studies

“Before you speak, listen. Before you write, think. Before you spend, earn. Before you invest, investigate. Before you criticize, wait. Before you pray, forgive. Before you quit, try. Before you retire, save. Before you die, give.” - William A. Ward

There are two glaring points that can be gleaned from the chart and quote above:

- The top three fears of retirees from age 50 – 70+ are financial concerns by a wide margin, and

- As William Ward intimates, critical thought must precede action

In summary, if one wants to avoid the realization of their greatest financial fears, it is never too early to start thinking critically and acting thoughtfully toward investing for future financial security. However, that is far easier said than done.

The most recent and impactful pain point that in some way or another affected everyone was the credit crisis of 2008. If you were primarily a real estate investor and decided that your exit point from the market was 2006, you won. If your exit point was planned for 2008, you were destitute. If you were “Warrenesque” and went long buying distressed debt and equities when blood was running in the streets, you have enjoyed the most robust bull market in history. That is the thing though…how many people do you know that went running into that burning building?

In my financial services career, it has been far more typical to see investors, despite all the logic, psychology and historical data I could muster to convince investors to “Buy Low & Sell High,” fear was the overwhelming influencer over their decisions. The perceived benefit of owning liquid investments is one of Wall Street’s most powerful allies because the Bigs know people, with or without the benefit of qualitative advice and planning, will almost always do the wrong thing. More wealth is transferred to Wall Street from Main Street in bear markets than bull markets.

In volatile, downward spiraling markets, private investors emotionally fatigued from climbing the wall of worry, eventually capitulate. They yield to the fear of losing everything and use the privilege of liquidity to sell out and effectively memorialize their paper losses into real losses. Buy high and sell low.

When institutional investors sense that Main Street has thrown in the towel, they step in at the trough and the wealth transfer cycle is now complete. Buy low and sell high. Two-thirds of every dollar in the markets are institutional dollars. Hedge Funds and other large institutional concerns have the gravitas to move markets to their benefit knowing full well that the Main Street Fear Factor will summarily win out.

Anecdotally and illustratively to the point, then Treasury Secretary, Hank Paulson announced in a press conference that the government would not allow a handful of very large banks to fail, Citi (C) amongst them. I picked up the phone and called one of my former clients and prefaced my next statement by saying, “My guess is that you are going to tell me I am an idiot for what I am about to say but I will remind you forever more that this will ultimately be the best advice you never took…Call your advisor and tell him you want to buy one-million Citi shares at $.86 in your IRA.” To which he replied, “You are right…you are an idiot!” Despite my primary argument that the US Government just said to the world, “The US Treasury is backstopping the banks,” his fear of losing any more of his principal was insurmountable. And his last statement was the icing on the cake. He said, “I’m getting off this roller coaster for a while…I’ll wade back in when I feel like market has stabilized.” Sell low and buy back in high later.

However, there is always a valuable lesson to be learned. The credit crisis taught the world that managing risk is tantamount to hopefully never feeling that kind of debilitating fear ever again. Particularly for those planning for or already in retirement, managing risk has an even deeper meaning because principal loss can no longer be replaced by re-entering the work force. Selling assets and self-imposed austerity measures in many cases are the only remaining options to recreate capital.

Necessity is the mother of invention. In the wake of the events that took place nearly a decade ago, innovation and thoughtfulness toward risk management has been a positive consequence of the pain and fear we all experienced.

The Senior Life Settlement Asset Class is an innovation that is now accessible to Registered Investment Advisors (RIAs) as a proven strategy to mitigate investment risk and predictably grow assets that intrinsically protects against principal loss.

Whenever one thinks about protecting themselves from risks in general, what is the first thing that comes to mind? Insurance. Insurance has always been a planning tool in place to transfer your exposure to various risks to another party in exchange for paying a premium for the right to made whole in the event of a loss.

Senior Life Settlements use the inherent characteristics of a life insurance contract as an investment vehicle to mitigate the risks associated with market volatility and potential principal loss that accompanies a fear-based trade. The typical strategies that risk-averse investors have traditionally deployed to address their fear of principal loss, like Treasury Bonds and Annuities, although safe, cannot produce adequate yield in the current protracted low interest rate environment to ameliorate the fear of outliving your money. Senior Life Settlements are a solution to address both risk and reward.

There is a lot to learn about this emerging new asset class, however, at the heart of the Senior Life Settlement value equation, there is one singular point to understand from which all other benefits radiate.

Simply put, life insurance is a contract. For a contract to exist, by definition, there must be bi-lateral consideration between at least two counterparties. Generally, they are the insured or policy owner and the insurance company. The consideration between the counterparties to the contract is that the policy owner pays periodic premiums in exchange for the insurance company’s promise to pay the contractual face amount of death benefit. Conceptually, that is pretty simple, right?

So, what is basic concept of a Senior Life Settlement? Well, it is a life insurance policy, with all contractual rights appertaining, that is transferred through a transaction between the policy owner and an investor. The insured sells their policy for an amount greater than what he or she would garner by surrendering their coverage to the life insurance company but less than the face amount. The purchaser assumes the responsibility for the payment of the premiums and at the passing of the insured, the purchaser is paid the death benefit as the policy owner. The purchaser gains because he or she earns the spread between the acquisition cost (Purchase price plus premiums) and the face amount.

The seller gains because he or she agnostically desires to sell their asset for as much as possible and the secondary or Senior Life Settlement market facilitates that outcome.

Here is the important part: as an investment, the capital creation mechanism is a contractual obligation of a highly-rated, US Legal Reserve Life (USLR) Insurance Company. There is no precedent of a failure by a USLR life insurance company to pay a legitimate claim in the industry’s history.

Senior Life Settlements can play a vital role in how an RIA can provide a solution to the source of that which resides at the heart of virtually all fears…the unknown. Because Senior Life Settlements do not create capital based on manager or market performance and because they avoid many of the risks associated with traditional market-based mechanisms, Senior Life Settlements in your investor’s asset allocations can effectively remove fear and consternation which is one of the primary tasks the advisor has been assigned the responsibility to remove from their clients’ financial lives.

Now that you understand the core value proposition of the Senior Life Settlement Asset Class, call Capstone Alternative Strategies at 404-504-7006 or email contact@capaltstrategies.com. There is a lot more to this story how Senior Life Settlements can help your RIA firm manage the Fear Factor.

Jason A. Bokina

Jason A. Bokina Jason Bokina is Director of Business Development for Capstone Alternative Strategies. He began his career with Harris Bank in operations, then moving to Northwestern Mutual in financial planning. After Northwestern Mutual, he was responsible for the startup and management of his own investment real estate company, Signature Real Estate Group, which helped provide the foundation for his involvement with alternative investments and the Senior Life Settlement space. Jason has extensive experience in sales, relationship management, marketing, and business development. He also has operational and managerial experience among a range of different industries. His primary role with Capstone Alternative Strategies is promoting and building the right strategic relationships for the US advisor Senior Life Settlement model. Jason graduated from Purdue University with honors, earning an undergraduate degree in Industrial Management.