Market dislocations occur all the time. Money managers, market strategists and traders seek these disruptions to create opportunities to buy and sell into and out of names with velocity. This can falsely lead investors to a euphoric feeling the markets will just keep going up and up and up.

The euphoria or what former Fed Chief Alan Greenspan referred to as “Irrational Exuberance” is what Main Street investors feel when markets go parabolic creating a herd mentality that is very hard to derail. The institutional investment community is quite adept at spotting these trends and leveraging them to their favor usually to the detriment of the retail investor.

You remember bubbles, right? Like the Technology Bubble in 2000. Investors couldn’t be dissuaded from paying share prices that were at nosebleed EPS multiples for companies with bloated valuations, no revenue, no earnings and as it were, no future. The irrational exuberance of blindly following a market that would seemingly never stop going up…defying gravity…then Blammo. The bottom falls out. Damn, didn’t see that one coming.

Or no-documentation-stated-income mortgage loans, exotic derivative voodoo and an endless supply of almost free money to stoke the fires. What could possibly go wrong? Besides a global credit crisis of course.

And now we’re here. Welcome to the CovidEconomy. As much as I would love to just go off on a bare knuckles rant here about the whole world changing, all that a reasonable person can conclude with absolute certainty is there is absolutely no certainty to be had. In other words, the beatings will continue until morale improves around here!

When these types of opportunities avail themselves (like right now), it’s certainly possible to profitably trade the waves or build positions on the dips if you and your advisor have those skills. It’s really not that tough. All you have to do is anticipate the movement of the markets’ ebb and flow, keep plenty of dry powder until you’re ready to pounce and time your trades opportunistically. Again, what could go wrong?

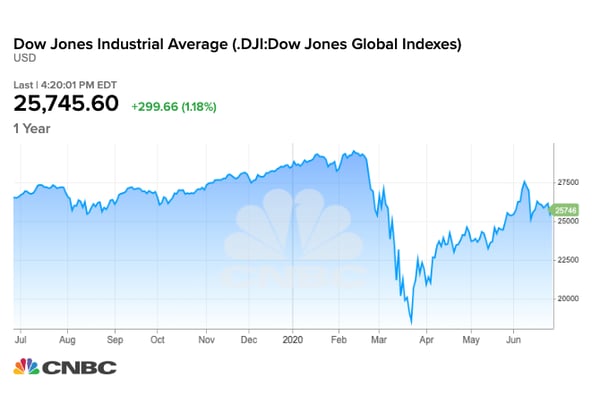

It’s like you could cut the sarcasm in the room with a butter knife! I am self-aware that a little angst might be seeping out in the form of passive-aggression here…it’s just to lighten a somber mood but seriously, this is what the Dow Jones Industrial Average looks like over the trailing 12 months.

The human toll that COVID may ultimately inflict on humanity has been horrifying to experience and to watch others experience. I strongly believe that the economic effect will be of a similar magnitude. The forced reordering of society is mutating the way we do business, making us resilient to new risks, becoming aware of new capabilities and generally stretching our collective comfort zones including the way we invest money.

In a former lifetime and a different industry, an axiom that was often bantered around was, “I wouldn’t do anything to you that I wouldn’t do for you.” Endearing, right? But to that point, market volatility, depending on which side of the market or a trade you’re on, long or short, helps and hurts at different times. A broken clock is also right twice a day.

To be clear, I’m not pitching doom and gloom here. To reiterate my stance on equities, bonds, real estate, currencies, precious metals, private equity, artwork, classic cars, loans, small business…they all serve the purpose of growing your wealth. They all have different benefits and exposures depending on the direction of the tides. But market and economic dislocations can, do and will come out of nowhere. We can’t do anything about this shitshow we’re in now, but we can certainly be prepared for the next one.

Managing volatility risk in your portfolio, whatever you own, is difficult when you’re over-weighted in high beta assets and the market moves adversely.

“The best way to reduce your exposure to market dislocations is to dislocate yourself from the market.”

I’m talking about building a contra-position in an alternative asset class that works independently of markets, negates low interest rates and most importantly, works differently than variable market pricing investment structures.

The mechanics and components are different. The bones of this asset class are what virtually eliminate the correlation coefficient to most risks that impact our economy.

“First, the asset backing the investment is a life insurance policy. Of epic importance to grasp here is that virtually all the economic and geopolitical risks that cause markets to move and asset prices to fluctuate have no effect on a life insurance policy.”

The general purpose of insurance is to provide protection against an economic loss. Life insurance is a contract where an insured pays premiums in consideration for a certain amount of death benefit stated on the contract’s face and payable by the carrier to named beneficiaries at the insured’s passing.

The life insurance industry may be the only peerless performer as stable financial industry segments go if track record and reliability are important (U.S. Legal Reserve System).

Unlike the perpetual nature of a company, a life insurance contract is limited by the lifespan of the policy owner. The policy’s maturity is the single triggering event that causes the distribution of the death benefit and the cashflows from the investment.

The difference or spread between the investor’s acquisition cost (purchase price plus premium reserve) is at a significant discount to the face amount of the policy. The spread is the investor’s Yield-to-Maturity. The spread does not change. The time to maturity of a policy is the only variable.

When multiple policies are aggregated in portfolios, investment risk within the portfolio are spread across a number of contracts with varying carriers, face amounts, life expectancy spreads, male to female ratios and other portfolio construction elements to achieve differentiation and balance.

The asset class is Senior Life Settlements. A diversified portfolio of secondary market life insurance policies positioned against other volatile assets in your overall portfolio will reduce volatility (beta) and stabilize returns (alpha).

Let me leave you with this. I’m sure most of you are familiar with performing some sort of Risk Tolerance analysis for a client to help them understand their own investing emotional quotient. The questions usually ask something like, “If you were to invest money in a basket of assets that could potentially go up by 25% next year, how much would you be willing to lose to make that return?”

That’s called downside capture rate. With a Senior Life Settlement, downside capture is eliminated. The policy pays out the face amount of the policy. No more, no less. There is no price volatility. Life settlements do not have to trade risk for return. Time is the only critical variable here and time applies itself equally to all investments. The only difference is that a Life Settlement can mature at any time and that upside surprise in times like these and those that will follow is comforting.

For more information on how Senior Life Settlements provide stability for your clients and prospects, call Jason Bokina at 404-504-7006 or send an E-mail message to Contact@CapAltStrategies.com.