In Part I, we talked about how what we like to call the “Chain of Custody” works to buy and own a home and how similarly a life settlement transaction is executed.

In both instances, you have a non-homogenous asset that must be evaluated for its own merits and the buyer and seller will transact based on their own subjective determination of value. Due diligence is key. You wouldn’t buy a home without looking at comparative prices, competitive mortgage rates and having a thorough home inspection performed.

Specialist counterparties play roles to facilitate various functions like escrow facility management, appraisal, title custody, etc. in order to protect the consumer. Makes sense, right?

I’ve used Mark Twain’s quote that appears at the beginning of the Movie “The Big Short” before and it bears repeating…

“It ain’t the things you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

It’s not too much of a stretch for any of us to remember how the wheels came off in 2008 when the Mortgage Meltdown happened. Incredible feats of financial manipulation in the forms of no-documentation loans, inflated appraisals, elaborate mortgage products and the like were being performed right in front of our eyes. Beside Steve Carell and Christian Bale, who knew?

I mean, it’s the American Dream to go deeply into debt to put a roof over your head. And so, we’ve been trained to believe in the real estate and mortgage banking industries so that we no longer question the efficacy and safety of the system. Hit the snooze button…everything’s gonna be just fine…do so at your own expense.

The bankers know full well, because they’ve trained us this way, that our brains only need to understand that I make more money than I need to make the monthly mortgage payment. Hey, rates went down a quarter of a point…let’s refinance!

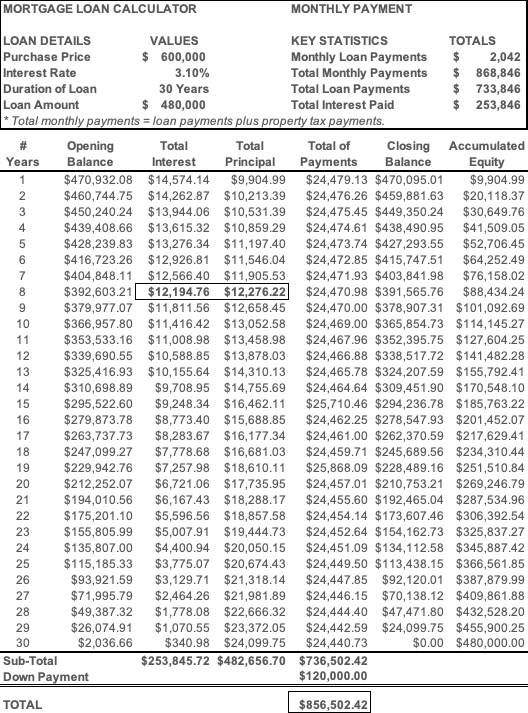

But, have you ever asked your mortgage banker to decipher an Amortization Schedule of your loan? An amortization schedule is a table detailing each periodic payment on an amortizing loan, as generated by an amortization calculator. Amortization refers to the process of paying off a debt over time through regular payments. But did you ever stop to think how much you’re actually paying or how you develop equity over time? Let’s take a look.

No one expects anything for free. Money has a cost to borrow it. No arguments there. But banks don’t take risk. Let’s take a look at where mortgage money comes from and where the risk is distributed.

First of all, the bank funds mortgage loans with the demand deposits money of its customer base. The bank pays a smaller amount of interest to the depositor and charges the borrow a greater amount then they pay out for the use of its depositors’ capital. The bank harvests a profit on the spread between the rates they pay their depositors and collect from their borrowers.

Second, the bank starts with a fully collateralized and personally guaranteed loan, usually at 80% (or greater depending on different circumstances) Loan to Value (LTV), or inversely, at a 20% equity position to reduce the risk of reselling a home in foreclosure.

Third, a mortgage loan is designed to pay the bank back the majority of its interest spread early in the loan cycle and the borrower is put at a disadvantage in terms of equity accumulation.

To summarize, it really costs over $850,000 to finance $480,000 with mortgage interest rates sitting at historic lows. The bank will collect over $107,000 or about 42% of its profits in the first 8 years of the mortgage. The borrower bears all the risk. There’s a very good reason why you don’t get a monthly statement about your home’s net worth.

From a financial perspective, there’s more counter-weighted risk on the borrower’s side than the lender’s. Right out of the gates, the total of payments is 143% of the purchase price. The cost of money, albeit at historic low rates, for your brand new shiny long-term liability is $24,000 per year plus the lost opportunity cost for the inability to redeploy your $120,000 down payment elsewhere.

Your home will have other costs like taxes, maintenance, insurance, repairs and maybe some upgrades over time. And, last there’s no guarantee that your home will appreciate in value.

That’s not much of a sales pitch and thus why the home lenders have packaged the whole thing in a nice, neat little American Dream box so you’ll be lulled to sleep and don’t have to think…the things you know for sure that just ain’t so.

Wealth, unless won or inherited, has a tendency to be earned by those that challenge conventional wisdom and prepare for opportunity. What is it Warren likes to say…

“The chains of habit are too light to be felt until they are too heavy to be broken.”

Following the herd has a cost. Making your own path takes courage and resolve. In the next and final installment of this blog, I will show you how to re-engineer a mortgage, put the pieces together separately, hedge real estate volatility risk and make the home purchasing process far more cash flow efficient.

Interested in learning more about Senior Life Settlements? Let's talk. Click below to ask further questions or to schedule an introductory call: