In the first two installments, we shared some information about how a life settlement transaction has similar facets to buying a home to help paint a familiar landscape for understanding the alternative nature of the asset class.

We learned that although a mortgage loan is certainly the easiest and most widely accepted method to fund the purchase of a home, the deck is stacked largely in the lender’s favor.

So, let’s take a look at what happens when you pull the pieces apart. In a conventional mortgage loan, the Principal and Interest elements of the loan are combined. Thus, this kind of multi-variant mathematical engineering is what allows them to work their magic. God bless’em.

If we treat Principal and Interest separately, there are cash-flow advantages and different risks that now apply. The type of arrangement I am speaking of is known as an Interest-only (“I/O”) loan.

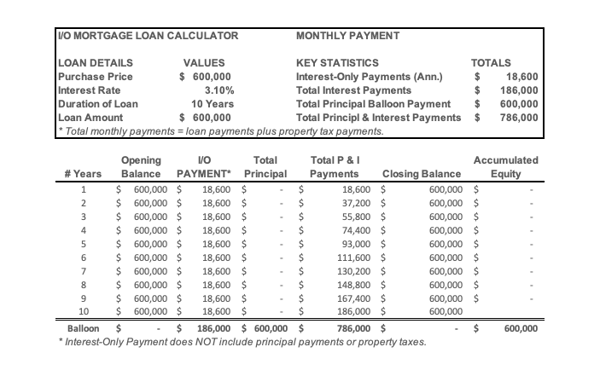

I/O loans are for the most well-healed and riskless borrowers. I/Os are often used on commercial real estate when the borrower wants to keep their mortgage payments as low as possible for cashflow efficiency and perhaps to maximize their leverage in a seller’s market (Also known as a Flipper’s market). Below is an extreme example of a Balloon Payment type of I/O loan for illustration’s sake.

Alright, what’s good and bad here? From a theoretical standpoint, nothing. Only people that don’t need to borrow money can get, or more importantly create, a loan like this. Assume the borrower is pledging securities and/or real property amounting to a multiple of the amount borrowed as collateral to quell the bankers’ disdain for risk.

The first and best achievement in this type of credit structure is taking control of how your money is allocated to manage the liability. By segregating the Principal & Interest elements of a mortgage loan, the borrower takes the control out of the lender’s hands and into his or her own. By being able to pay interest-only when cash is scarce or has a higher return elsewhere, the borrower can tip the scales in whichever direction is most self-advantageous.

Low interest rates, another housing bubble, another technology bubble, high unemployment, mounting commercial real estate defaults and a volatile stock market are a reflection of the unprecedented fiscal and monetary support provided by the Federal Government, aka the “Fed Put.”

The Fed Put is the widespread belief that the US Federal Reserve will always rescue the economy by decreasing interest rates. The term originates from the analogous comparison of selling a put option on the market.

The last notable iteration of the Fed Put as you may recall from the credit crisis was when Treasury Secretary Hank Paulson issued the edict that the US Government was basically nationalizing the five “Too Big to Fail” banks and proceeded to flood not just the US economy with liquidity, but the worlds. I’ve seen it noted that the final tally was in excess of $22 Trillion. That will ultimately come home to roost in higher taxes and price inflation. In the absence of a healthy fixed-income market, alternative safe yield is attractive. I’m a realist. Not a catastrophist. In chaos comes opportunity.

To deploy assets and manage liabilities as I shall illustrate is one look at how to maximize cash flow efficiency and keep all of your assets working as hard as possible while minimizing and retiring liabilities efficiently to build a stronger personal balance sheet.

My first thought is, can I make a high enough return on my investable assets to cover the cost of money to borrow? In other words, can I make those assets and liabilities cancel each other out?

And in my next synapse, how can I cover the risks? What if rates go up, home prices and the stock market go down? You know, rich people problems. And let’s keep in mind, this idea is strictly a thought starter. This is an idea for those with the capital, income and acumen to move their men around the chess board to position Checkmate when the markets involved provide an opportunity such as prolonged low interest rates and abundant liquidity.

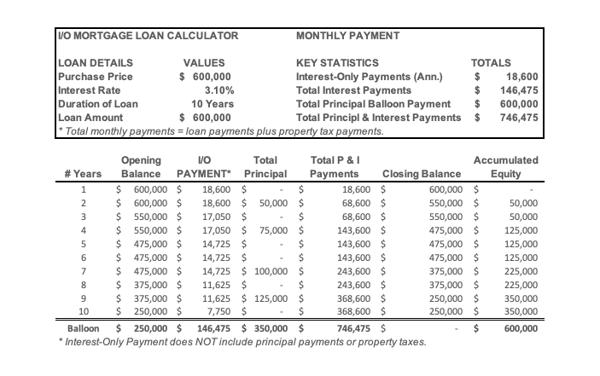

The elephant in the room, of course, is the outstanding principal of the interest-only loan. By separating the Principal and Interest components in a loan, three things happen:

- Every dollar paid in excess of the interest payment reduces principal by one dollar.

- Every dollar paid in excess of the interest payment increases equity by one dollar.

- Every payment decreases with every dollar reduction in loan principal outstanding.

Let’s say that in the example below, the borrower saw fit to make additional drop-ins of payments to principal in years 2, 4, 7 & 9. If the borrower believes the ROI on real estate is the best return on investable capital, this makes sense.

Alright, now let’s focus on those principal payments. You have to repay the loan at some point. How are you going to generate the cashflow to make principal reductions along the way? Maybe it will come from market gains, personal income and assets or perhaps the plan is to let the real estate appreciate in price while fully encumbered. If the stars align, any of the above can work. Or not. Again, this is not for faint at heart.

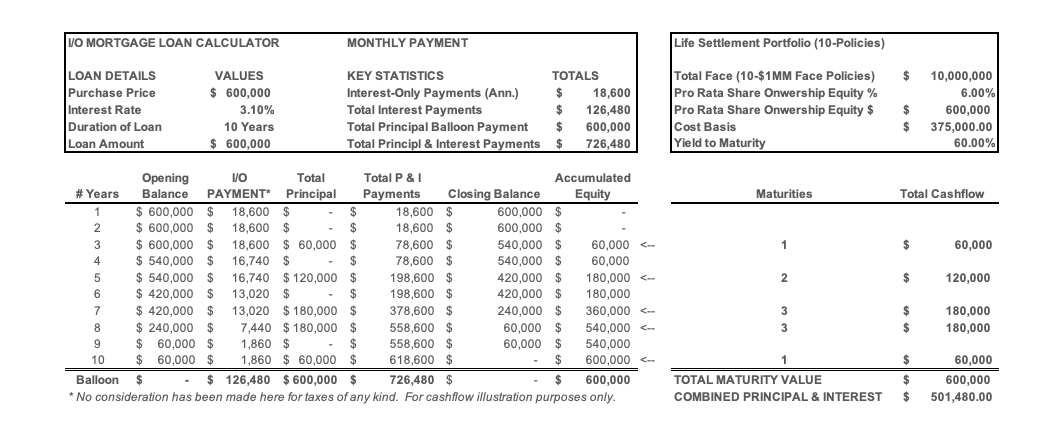

Or, you could allocate a portion of your investable assets to acquire a diversified portfolio of life settlements to provide a sinking fund to create the cashflow to retire the loan…using discounted dollars. Manage the risk and keep all of your assets working.

Let’s look at our I/O Loan table again but with a series of cashflows from policy maturities in a portfolio of life settlements designed to automatically retire the loan.

Now, you’ve carved out the corresponding stock market risk in an absolute return vehicle equal to the loan debt. If the value of your stocks decline precipitously, you’re not dependent on gains to retire loan principal. The cashflow from policy maturities reduce principal, lower interest payments and increase equity. The life settlement portfolio and the loan principal offset one another.

The ability to pay only the interest component in lean years when income is stretched is beneficial if earned income tends to vary. You have complete discretion to allocate more or less capital to principal as desired.

Most importantly, you now have a discounted cashflow mechanism in place to liquidate the loan debt of $600,000 with only $375,000 of your own capital. Of course, you have to manage the interest payments on the loan until the portfolio matures from your own capital and income sources but that’s the same no matter how you finance the liability.

If the scenario were to play out as illustrated above, the total of principal and interest payments to retire the loan is $501,480. Additionally, if the life settlement cashflows can be deployed elsewhere and it’s to the borrower’s advantage not to pay down debt/buy up equity, that option is readily available and you don’t have to refinance your home or take out a home equity loan to get your dough.

This financing structure can get even a little sportier if you are in position to be your own bank. Securities-Backed lines of credit are offered by most investment platforms and their rates to advance against pledged securities could be significantly lower than the mortgage market. According to recent attestations from the Federal Reserve, rates shall remain suppressed at or near zero at least until 2023.

To close, I am a huge fan of keeping powder dry and looking for market dislocations that can be profitably arbitraged. I am also a fan of keeping as many controllable variables under my command as possible. By dis-integrating the components of a mortgage and pairing a portfolio of life settlements to create the cashflow to automatically retire the loan, you maximize cashflow efficiency and hedge risk.

Total of Payments to buy the same $600,000 house:

- Conventional 30-Year Fixed Rate Mortgage = $856,502

- Interest-Only 10-Year Balloon = $786,000

- Interest-Only 10-Year Term with Life Settlements = $501, 480

And now the best part, if everything works against you, you can always just go get a mortgage.

Interested in learning more about Senior Life Settlements? Let's talk. Click below to schedule an introductory call: