Recently, I saw in a news post on my CNBC app that the US Treasury Two-Year Note and Ten-Year Bond yields flattened which means long-term and short-term debt yields are converging. What does that mean? When money moves heavily into US Treasury Instruments in what the financial press monikers as a “Flight to Safety,” it usually signals a “Risk-Off” trade to preserve capital until the uncertainty and associated volatility (beta) of riskier asset classes become more well-defined and money managers feel a greater degree of comfort to go back into “Risk-On” positions in search of higher, risk-adjusted returns (alpha). As a reference point for fixed-income instrument risk-adjustment analysis, the 10-Year Treasury Bond is considered the “Risk Free” rate as Treasuries are backed by the “Full Faith and Credit of the US Treasury.”

As reported by CNBC3, the difference between committing capital for 2 years (US 2-Year Note Yield 1.29%) or 10 years (US 10-Year Treasury Bond Yield 2.46%), only yielded an additional 1.17%. Simply put, adequate, safe yield in the current protracted low interest rate environment is very hard to find even when you are willing to commit to a longer time horizon. The major equity markets are setting new all-time highs almost daily, there are further Fed interest rate hikes in queue, geo-political challenges abound and myriad other catalysts are effecting market volatility and increasing uncertainty. That’s what I gleaned from ten minutes of reading the CNBC News Feed on my phone.

For Registered Investment Advisors (RIAs), Fee-Based Planners, market analysts and others in the investment advice business, risk mitigated asset allocation has become more difficult than ever before. Quantitative Easing, amongst other measures taken by the government to reflate the economy by creating a low interest rate environment to spur investment, employment and economic growth in general has changed the way traditional fundamental and technical analysis of market economics must be approached.

A market dislocation exists that can exploited to defend against the adverse effects of these endemic paradigm shifts, particularly as it applies to risk management. It’s called the Senior Life Settlement Market.

The Senior Life Settlements Asset Class is an anomaly that is agnostic and apathetic to almost everything that makes other market-based investment mechanisms twitch every time Jim Cramer hits the “House of Pain” button on his control console. Senior Life Settlements remove the pain points of correlation, overlap, market timing, yield curves, order of returns, etc. out of the equation and relegate the primary risk of time to policy/portfolio maturity and illiquidity as the only remaining elements to pricing the risk of owning the Life Settlement asset class.

A Senior Life Settlement is an asset that derives its value or yield from the contractual obligation of a highly-rated US Legal Reserve2 Life Insurance Carrier. The spread between the acquisition cost and the face amount of a life insurance policy is the store of value for the investor. When an insurance policy owner decides to sell their policy to a third party, the new owner assumes the obligation to pay premiums and all the rights appertaining to the contract transfer to the new owner in kind.

You are a Registered Investment Advisor. You are endeavoring to be a responsible caretaker of your clients’ best interests as it relates to their financial stability and aspirational objectives. Try as you might to anticipate the unforeseen and apply risk mitigation strategies to protect your clients’ principal while searching for alpha, but there is only so much one can control. Senior Life Settlements represent an opportunity to use an intelligent solution to address many of your investment risk management challenges in client asset allocation that does not require any active management.

As a tool in your cadre of products and services, Senior Life Settlements can play a vital role in an RIA’s mission to grow your clients’ asset base as safely as possible. It is important to understand the distinctions between the “Risk Free Rate” of a Treasury Instrument for those investors that are maximally risk averse and Senior Life Settlements. Senior Life Settlements are an alternative fixed-income asset class that provides utility to protect principal, mitigate risk and reduce portfolio volatility while also serving to grow your firm’s Assets Under Management (AUM) as a coefficient of growing your clients’ wealth on a permanent and predictable basis.

FOR ILLUSTRATIVE PURPOSES ONLY

1 http://www.investopedia.com/terms/f/full-faith-credit.asp

3 CNBC - 10-Year Treasury Bond Yield of 2.46% quoted within the table was as of 03/22/17.

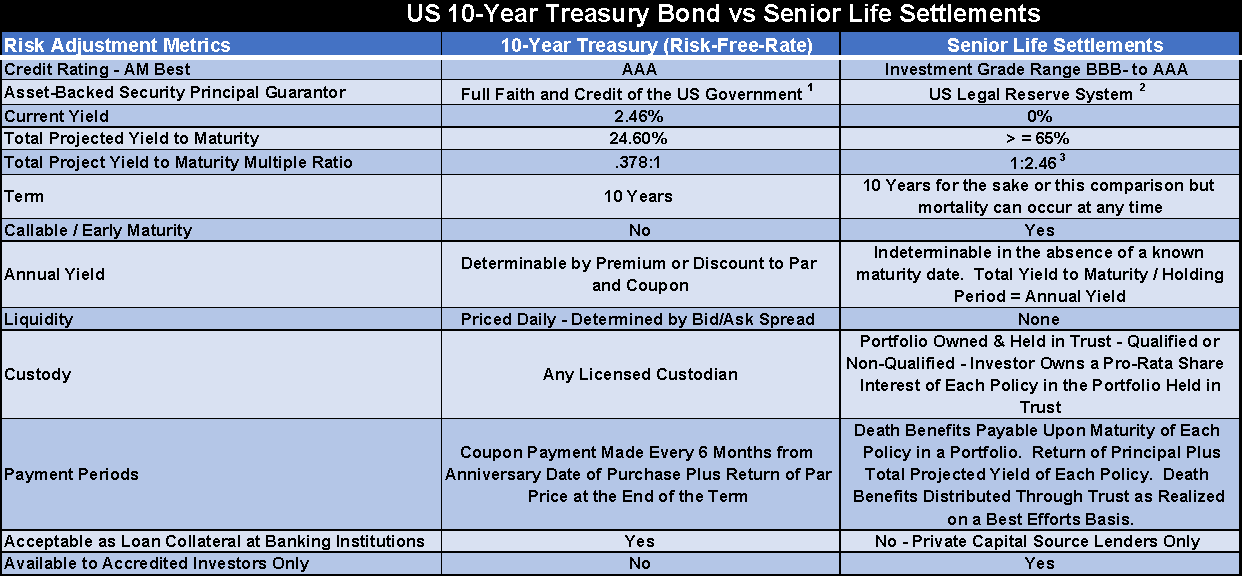

The most notable differences to which one should draw attention in the chart are the following:

- The 10-Year US Treasury Bond is Backed by the Full Faith & Credit of the US Government and is considered the “Risk-Free-Rate” and the comparison point by which fixed-income instruments are qualified to evaluate credit default risk and principal safety in general.

- The US Legal Reserve System (USLR is the charter under which US Life Insurance Companies operate to ensure the ability to pay death benefits as they come due. There is no documented precedent that a USLR life carrier has ever failed to pay a legitimate claim on a life insurance policy in force and good standing at the time of an insured’s passing.

- The comparison chart infers from the Yield to Maturity ratios that both the 10-Year US Treasury and the Senior Life Settlement Asset Classes, compared-and- contrasted therein, are both held for the same 10-year holding period. It should be noted that Senior Life Settlements can mature at any time (before, at or beyond the mean Life Expectancy) which would change the Yield characteristics presented in the chart. The projected holding periods of a Senior Life Settlement are assessed by medical underwriters that produce a Mean Life Expectancy which acts as both a pricing mechanism in the Secondary or Senior Life Settlement Market and as an estimated holding period to maturity. Life Expectancies are not guaranteed as human mortality cannot be accurately predicted. The chart is for Illustrative Purposes Only.

- Treasury instruments provide for daily liquidity priced by independent market makers based on bid and ask prices reflected in the fixed-income markets at the time of the liquidation. By contrast, Senior Life Settlements are illiquid and there is no established market for an orderly or timely liquidation of a contract or portfolio. As can be seen from the Yield comparisons, Senior Life Settlements offer an attractive Illiquidity premium in exchange for the lack of marketability.

In the quest for adequate, risk-adjusted yield in the current economic climate where suitable options are scarce, market stability is tenuous and the international political landscape is changing virtually hour-by-hour, asset allocation strategy requires innovative thought leadership to ring fence a more elaborate set of investment risk considerations than most financial advisors have ever faced before. The Senior Life Settlement alternative asset class uniquely leverages the power of life insurance in an asset-backed security supported by an industry charter that has performed flawlessly for over one-hundred and fifty years.

If a risk-averse investor had adequate principal to produce a desirable level of income to maintain the lifestyle to which they have become accustomed investing only in riskless Treasury investments, one would. For the rest of us, the risk/return conundrum shall persist.

If you are a Registered Investment Advisor seeking to maximize your firm’s value proposition and differentiate your practice from the competition, Senior Life Settlements share some similar characteristics with Treasury instruments that can be thoughtfully applied to your RIA Firm’s asset allocation strategy. More alpha and less beta is the order of the day. The Capstone Platform is an exclusive, turnkey solution to give you access to this innovative, utilitarian asset class to deliver real, quantifiable results to your clients. Be the change agent and thought leader to whom your clients have dedicated their financial well-being under your expert guidance and governance.

For more information, please contact Jason Bokina at (404) 504-7006 or email us at contact@capaltstrategies.com.

Michael J. Bradburn

Michael J. Bradburn Michael Bradburn started his career as President and General Manager of a small automotive sales conglomerate, where he oversaw and managed several domestic and Asian manufactured retail dealerships. After selling the dealerships, Michael then worked with Prudential Preferred Financial Services in life insurance and annuity sales. He later advanced his career in private wealth management at Morgan Stanley-Dean Whitter and subsequently Merrill Lynch. Following that, Michael served as Chief Financial Officer of a metals manufacturing and distribution startup, where he was instrumental in securing patents and developing a completely virtual, vertically integrated, manufacturing and distribution technology serving the global powder metallurgy industry. At Capstone Alternative Strategies, he oversees marketing and advisor development. Michael attended Indiana University where he became a member of the Sigma Chi fraternity and later earned his BS from Ball State University.