The Yale endowment is a perennial heavyweight amongst the mammoth Ivy League endowments. We are big fans of the Yale money management Illuminati in New Haven. What’s behind their legendary success, beside unlimited intellect and resources, might surprise you.

Yale's long-term success sits firmly at the top of the leader board amongst top-flight institutional investors. In the 10-Year period ending June 30, 2020, the endowment earned an average annual return of 10.9%. There must be something to that whole “Rule of 72” thing. During that time period, the endowment’s asset base nearly doubled from $16.7 billion to $31.2 billion. That’s no decade-long, bull market fluke. The Bulldogs have been getting it done for a long time. The 20-Year performance number is 9.9%.

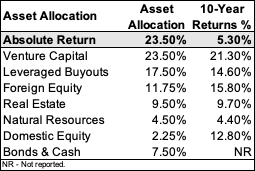

Take a look at where they put their money.

Does the Yale’s 2021 target asset allocation surprise you? It did me too. Over half of the portfolio is weighted in asset classes with less correlation to publicly-traded-markets than the other buckets. Almost a fourth of the portfolio is invested in Absolute Return. Let’s talk about that.

So, what is an Absolute Return asset class, why do I want it and how do I get it?

The absolute return is a measure of the gain on an investment portfolio expressed as a percentage of invested capital. A zero-coupon bond works much like this in that one buys the bond at a discount to its face and holds the bond to maturity. The absolute return, the discount to face or spread, is known in advance.

Absolute return assets are predominantly asymmetrical and non-correlated to volatile markets. They don’t look or act the same way as stocks and bonds and it’s in these mechanical dissimilarities that tremendous value can be extracted. Increasing exposure to absolute return and other hard assets is how the Yale endowment has outpaced a raging bull market while limiting downside-risk deploying assets away from the markets.

So, without the brain trust and capital base of a storied multi-billion-dollar academic juggernaut behind you, how do you employ the same thought process in an individual investor’s asset allocation?

An example of the aforementioned absolute return vehicle would be the Life Settlement asset class. Life Settlements act as a hedging mechanism to offset the risks against a volatile basket of securities. Life Settlements can perform the function of balancing a portfolio in the absence of a healthy functioning fixed-income market.

The spread between the investor’s cost basis and the face amount of the contract is the Yield-to-Maturity or Absolute Return and is known in advance. Life settlements are agnostic to market pressure, averse to geo-political upheaval and unaffected by real or surreal circumstances as the case may be. Thank goodness nothing like that is going on right now.

As an advisor, investors are looking for guidance and innovative ideas to help build and protect wealth. The Senior Life Settlement story will help differentiate you from competitors. If you’re ready to take your practice to the next level and offer your clients a non-correlated investment opportunity with absolute returns, we should talk. For more information, call Jason Bokina at 404-504-7006 or email contact@capaltstrategies.com.